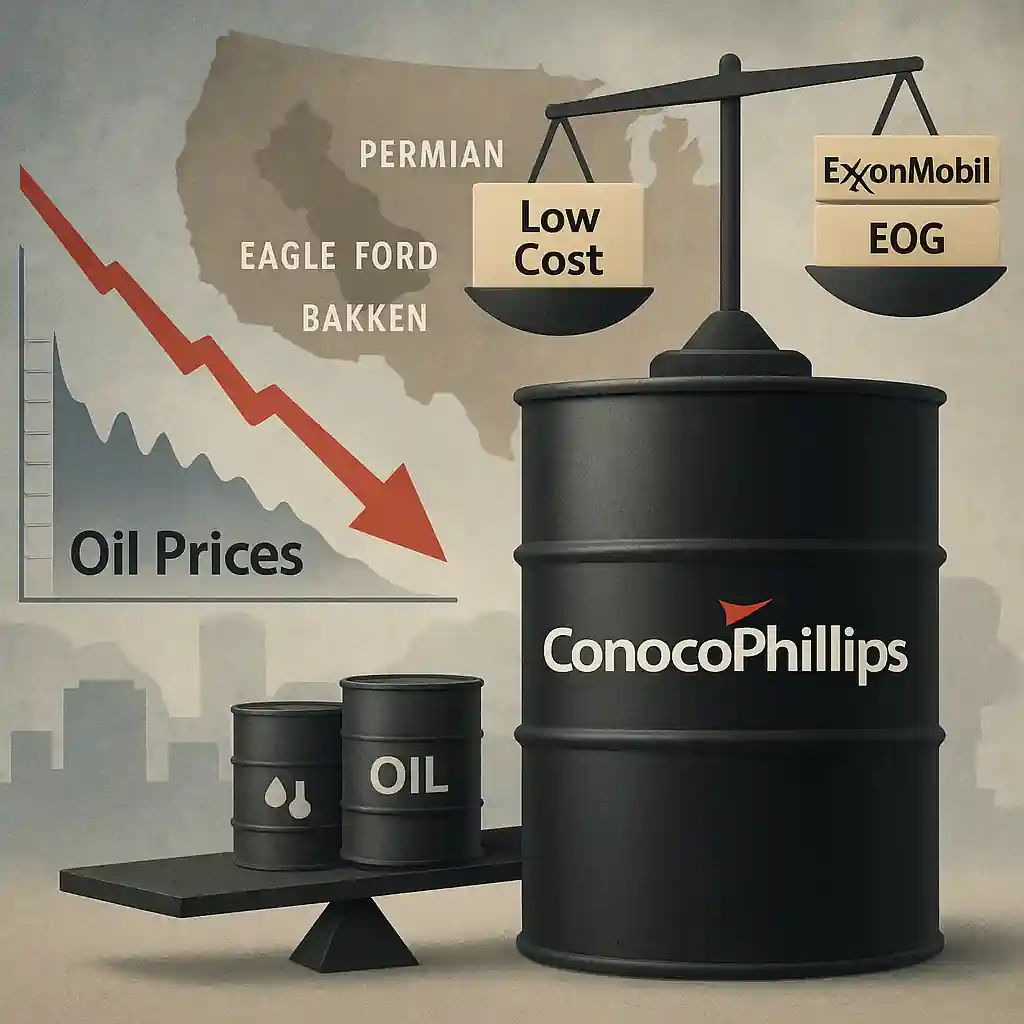

ConocoPhillips Stands Strong in Low Oil Price Cycles

ConocoPhillips (COP) boasts a powerful edge in the oil market. Its drilling costs are well below $40 per barrel. This gives the energy giant a rare ability to maintain profitability even when global oil prices tumble. Unlike many upstream players, COP can produce oil cheaply across multiple key U.S. shale basins.

Strategic Assets in Major U.S. Oil Plays

COP’s operations span the prolific Lower 48 shale regions, including the Permian, Eagle Ford, and Bakken formations. These oil-rich areas offer vast, low-cost reserves that support long-term output. This geographic spread enhances production stability and reduces reliance on any single region.

Immune to Oil Price Volatility

With break-even costs so low, ConocoPhillips is largely shielded from oil price swings. The company can operate profitably when oil trades at $65 per barrel, or even lower. This strategic advantage helps maintain steady cash flow regardless of market turbulence. For investors, that’s a reassuring sign of resilience.

Investor Confidence Supported by Consistent Output

ConocoPhillips continues to deliver amid price uncertainty. Its ability to generate profits at lower oil prices places it ahead of many competitors. While other firms may scale back operations when prices dip, COP keeps pumping—delivering value through every market phase.

ExxonMobil and EOG Also Preparing for Oil Downturns

ExxonMobil (XOM) and EOG Resources (EOG) have also taken steps to mitigate oil price pressure. XOM aims to lower its break-even cost to $35 per barrel by 2027, and as low as $30 by 2030. That would make its oil production highly efficient and boost long-term margins.

EOG relies on a strong balance sheet to weather potential oil downturns. Even if prices fall below $45 per barrel, EOG expects to maintain operational stability using financial discipline. Both companies show foresight—but COP currently holds the cost leadership position.

ConocoPhillips Valuation Signals Market Confidence

Over the past year, COP shares have dipped 19.1%, slightly underperforming the broader industry average of -16.7%. However, the company’s EV/EBITDA ratio stands at 5.02X—well below the industry average of 11.15X. This suggests a relatively attractive valuation based on earnings power.

Strong Fundamentals Reinforce Oil Market Position

The Zacks Consensus Estimate for COP’s 2025 earnings has remained stable in recent days. This reflects confidence in the firm’s future, even amid oil price uncertainty. With steady estimates and operational efficiency, COP looks poised to lead through volatile times.